Open an Irish bank account while renting: 2026 guide

13 July 2026

11 min read

Learn how to open an Irish bank account renting your home. Our 2026 guide offers a step-by-step approach to simplify the process.

Opening an Irish bank account while renting is achievable with two core documents: valid photo ID and proof of your Irish address. For expats and new residents, this process sits at the centre of a frustrating loop. Banks want proof of address before they open an account, and landlords want bank details before they finalise a lease. Knowing how to break that cycle, and which documents work as alternatives, is the difference between settling in quickly and spending weeks in limbo. This guide walks you through the exact requirements, a practical step-by-step process, and the fastest way to get your finances and tenancy aligned.

What documents do you need to open an Irish bank account?

Most Irish banks require one original photo ID and one original proof of address for residents. Non-residents generally need two forms of each. That stricter standard catches many new arrivals off guard, so prepare extras from the start.

Acceptable photo ID

Passport (most widely accepted)

Irish or EU driving licence

Irish Residence Permit (IRP card)

National identity card (EU citizens)

Acceptable proof of address for renters

Utility bill dated within the last three months

Signed tenancy agreement showing your Irish address

Employer letter confirming your place of work and home address

Official government correspondence (Revenue, Department of Social Protection)

Document type

Examples

Validity

Photo ID

Passport, driving licence, IRP card

Must be current and unexpired

Proof of address

Utility bill, tenancy agreement

Dated within 3 months

Alternative proof

Employer letter, government letter

Dated within 3 months

Non-resident extras

Two of each category above

Same validity rules apply

One detail many renters miss: your name and address must appear identically across every document you submit. Inconsistent paperwork severely delays account approval. If your tenancy agreement uses "Apt" and your employer letter uses "Apartment," ask for a corrected version before your bank appointment.

Related Topics

#open irish bank account renting#how to open bank account in Ireland#requirements to open Irish account#banking options for renters in Ireland#opening a joint account in Ireland#Irish bank account for tenants

Related Articles

Pro Tip:Collect every piece of post that arrives at your Irish address, even junk mail from Revenue or local councils. Official correspondence counts as proof of address and costs you nothing to gather.

You will also need an Irish mobile number. Banks use SMS verification during setup and ongoing communications. Without an Irish SIM, you cannot complete the verification steps for most banking apps or branch processes.

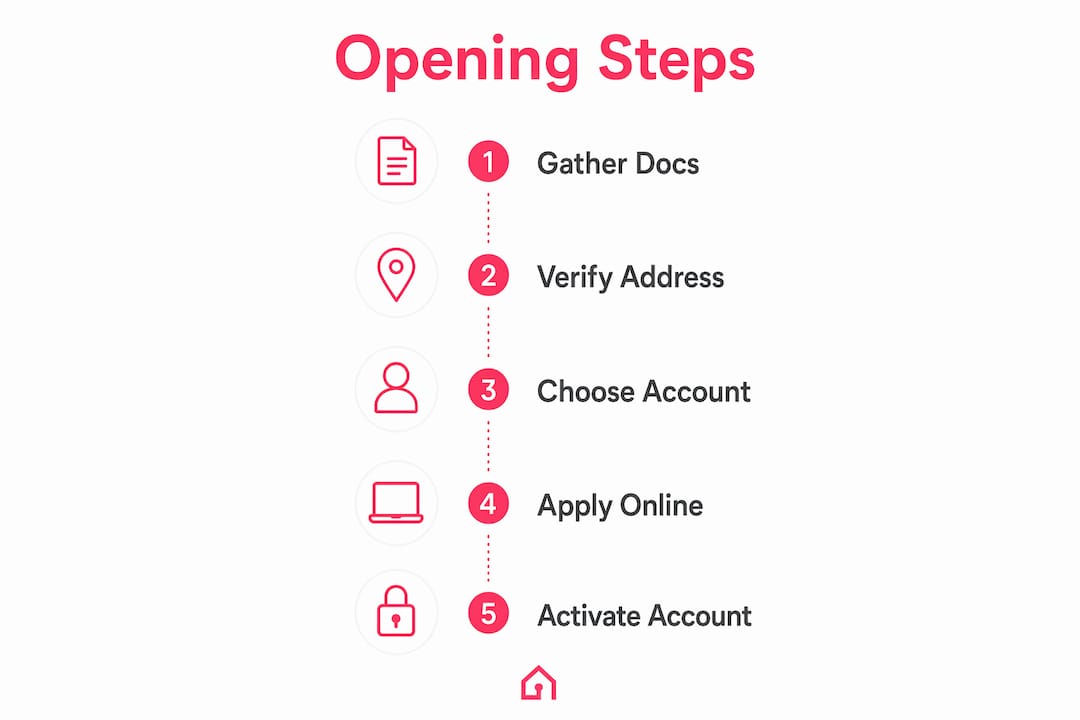

How to open an Irish bank account while renting: step by step

The process works best when you treat it as two parallel tracks: get a digital account running immediately, then build toward a traditional bank account as your documents accumulate.

Get an Irish SIM card within your first 72 hours. An Irish mobile number is required for SMS verification during banking setup. Buy a prepaid SIM from any supermarket or phone shop on arrival. This single step unblocks everything that follows.

Open a fintech account for immediate needs. Digital banks such as Revolut or Wise allow new arrivals to open accounts and manage rent deposits within days, whereas traditional banks can take 2–4 weeks after documentation submission. Use your fintech account to receive your first salary, pay a holding deposit, and show a landlord you have a functioning account.

Gather every proof of address document available. This includes your signed tenancy agreement, any employer letter confirming your address, and any official post. If you are in temporary accommodation such as a hostel or Airbnb, ask the host for a written confirmation of your stay. Some banks accept this for newcomers.

Book a branch appointment early. Do not wait until your documents are perfect. In-person meetings speed up verification and reduce document-related delays, particularly for international arrivals. Book the appointment the same week you arrive, even if you plan to gather more documents before attending.

Attend the appointment with originals, not copies. Banks will not accept photocopies or screenshots. Bring every document in physical, original form. If a document is in a language other than English, bring a certified translation.

Apply for your PPS number in parallel. Applying for your Personal Public Service number alongside your bank account avoids future amendments. Your PPS number is required for payroll and long-term financial activity in Ireland. You can add it to your bank account once it arrives, but starting the application early prevents delays to your first payslip.

Pro Tip:Ask your employer to issue a letter on headed paper confirming your start date, job title, and home address. This single document can serve as both proof of employment and proof of address at most Irish banks.

Check your bank's specific requirements before attending. Some banks publish their accepted document lists online, and requirements vary slightly between institutions.

How do you break the bank account and rental proof of address loop?

The circular problem is real. Banks want a local address to open an account, and landlords want local bank details to finalise a lease. Fintech accounts help break this loop temporarily, but you still need a strategy for the traditional banking side.

The most effective way to break the proof of address loop is to combine a fintech account with a draft lease or employer letter. Together, these two documents satisfy most landlords and give you enough to begin a traditional bank application simultaneously.

Here are the practical steps to cut through the cycle:

Use your draft or signed lease as proof of address. Banks may accept tenancy agreements as temporary proof of address for newcomers without established utility bills. Ask your landlord to sign the agreement before your bank appointment, even if the tenancy has not yet started.

Request an employer letter on day one. If you have a job offer or contract, ask HR for a letter confirming your Irish address. This works at most banks and costs nothing to obtain.

Use temporary accommodation documents. A written confirmation from a hostel, guesthouse, or short-term rental host can serve as a stopgap. Pair it with your passport and a draft lease for the strongest possible application.

Hoard official post. Any letter from Revenue, the Department of Social Protection, or a local authority carries weight. Keep every envelope.

Schedule your branch appointment before you feel ready. Preparation of multiple supporting documents and early scheduling reduces delays. Banks can tell you exactly what is missing during the appointment, which is faster than guessing from home.

The key mindset shift is this: you do not need a perfect set of documents to start. You need enough to open a conversation with the bank, and a fintech account to keep things moving while that conversation unfolds.

What types of bank accounts suit renters in Ireland?

Renters in Ireland have two main categories to choose from: fintech accounts and traditional high-street bank accounts. Each has a different role in your financial setup.

Fintech accounts

Fintech accounts from providers such as Revolut or Wise are the fastest option for new arrivals. They open within days, require minimal documentation, and give you an IBAN you can use for rent payments and salary deposits immediately. The trade-off is that some landlords and employers prefer a traditional Irish bank account, and fintech providers are not always accepted for direct debit mandates.

Most banks in Ireland do not charge fees to open an account, but may charge monthly maintenance or transaction fees. Government stamp duty applies at low levels on debit card purchases and ATM withdrawals. Fintech accounts often carry lower fees overall, which matters when you are managing a deposit and first month's rent simultaneously.

Traditional high-street bank accounts

Traditional accounts take longer to open, typically 2–4 weeks from documentation submission, but they carry more credibility with landlords and employers. They also support a wider range of direct debits, which you will need for utility bills and standing orders. Once open, a traditional account is the more practical long-term tool for renting in Ireland.

Joint accounts

Joint accounts are available for tenants sharing rental obligations, but require additional documentation and approvals similar to single accounts. Each applicant must supply individual ID and address proofs. If you are moving in with a partner or housemates and plan to share rent payments, a joint account simplifies the process, but factor in the extra time needed to gather documents for all applicants.

Pro Tip:Open a fintech account first and use it to pay your deposit and first month's rent. This gives you a transaction history, which some banks accept as supporting evidence of your Irish address when you apply for a traditional account.

Account type

Time to open

Best for

Key limitation

Fintech account

Days

Immediate rent payments, salary

Not always accepted for all direct debits

Traditional bank account

2–4 weeks

Long-term renting, employer payroll

Slower setup, stricter documentation

Joint account

2–4 weeks

Shared tenancies

Requires full documentation from all applicants

For most renters arriving in Ireland, the right approach is to open both. Use a fintech account to cover your first weeks, then transition to a traditional account once your documents are in order. You can find more context on the costs you will be managing in Hauzed's guide to rental costs in Ireland.

Key takeaways

Opening an Irish bank account while renting requires a two-track approach: start with a fintech account for immediate needs, then build toward a traditional bank account using your tenancy agreement, employer letter, and consistent documentation.

Point

Details

Two documents required

You need valid photo ID and proof of Irish address; non-residents need two of each.

Fintech accounts bridge the gap

Digital banks open within days and cover rent deposits while your traditional application is pending.

Employer letters are underused

A letter on headed paper confirming your address satisfies most banks and landlords simultaneously.

Consistency matters

Name and address must match exactly across every document or approval will be delayed.

Start the PPS number early

Apply for your PPS number in parallel with banking to avoid payroll delays later.

The part nobody tells you about banking and renting in Ireland

At Hauzed, we work with renters arriving in Ireland every week, and the same mistake comes up repeatedly: people wait until everything is perfect before they act. They wait for the utility bill. They wait for the PPS number. They wait until they have a signed lease. By then, two or three weeks have passed, and the rental they wanted has gone to someone who moved faster.

The Irish rental market, particularly in Dublin, does not reward patience. It rewards preparation. The renters who settle in quickest are the ones who get an Irish SIM on day one, open a fintech account before they even land, and book a bank appointment for their first available weekday. They walk into that appointment with a draft lease, an employer letter, and their passport, knowing the bank may ask for more. That is fine. The appointment itself moves the process forward.

The other thing worth saying plainly: do not send sensitive documents through WhatsApp, email, or any informal channel. Your passport, payslips, and bank details should only travel through secure, verified platforms. If a landlord or letting agent asks you to send these documents informally, treat that as a warning sign. Legitimate rental processes have proper channels for document sharing, and protecting your data from the start is as important as getting the account open. If you are searching for rentals in Ireland, Hauzed's guide to renting remotely risks explains exactly why informal channels create unnecessary exposure.

— Hauzed

Renting in Ireland with confidence starts here

Finding a verified rental and getting your finances in order are two sides of the same process. Hauzed is a trust-first rental marketplace built for exactly this situation. You can browse verified rental listings in Dublin and across Ireland, connect with landlords through a structured platform, and build a stronger tenant profile before you apply.

Hauzed is free for tenants. You can search listings without an account, then verify your identity and complete your profile when you are ready to apply. For new arrivals working through the banking and tenancy process simultaneously, having a verified rental profile gives you a real advantage in a competitive market. Start your search on Hauzed's rental platform and approach your next application with a stronger foundation.

FAQ

Can I open an Irish bank account without proof of address?

Banks may accept employer letters or signed tenancy agreements as alternative proof of address for newcomers who do not yet have utility bills. Combining these with a fintech account gives you a workable solution while you wait for traditional documentation.

How long does it take to open a bank account in Ireland?

Fintech accounts are typically functional within a week. Traditional high-street bank accounts can take 2–4 weeks from documentation submission, depending on the bank and the completeness of your paperwork.

Do I need an Irish mobile number to open a bank account?

Yes. Most Irish banks and banking apps require an Irish mobile number for SMS verification. Get an Irish SIM card within your first 72 hours of arrival to avoid delays in the account setup process.

Can I open a joint account in Ireland as a renter?

Joint accounts are available for tenants sharing rental obligations. Each applicant must provide individual photo ID and proof of address, so factor in extra preparation time if you are applying with a partner or housemate.

Do I need a PPS number to open an Irish bank account?

You do not need a PPS number to open a basic account, but applying for your PPS number in parallel with your bank application avoids amendments later. Your PPS number is required for payroll and long-term financial activity in Ireland.