Discover what deposit protection means for renters. Learn how it safeguards your money and ensures a hassle-free renting experience!

Deposit protection is the legal requirement that a landlord must place a tenant’s deposit into a government-approved scheme or insured arrangement to keep it safe throughout the tenancy. Under UK law, landlords have 30 days from receiving a deposit to protect it and provide written confirmation to the tenant. Two main types of scheme exist: custodial, where a third party holds the money, and insured, where the landlord retains the funds but pays for insurance cover. Understanding what deposit protection means is the first step to avoiding disputes, protecting your money, and renting with confidence.

How do deposit protection schemes work?

Deposit protection schemes are the formal systems that hold or insure tenant deposits during a tenancy. They exist to prevent landlords from unfairly withholding money at the end of a let, and to give tenants a clear route to reclaim what they are owed.

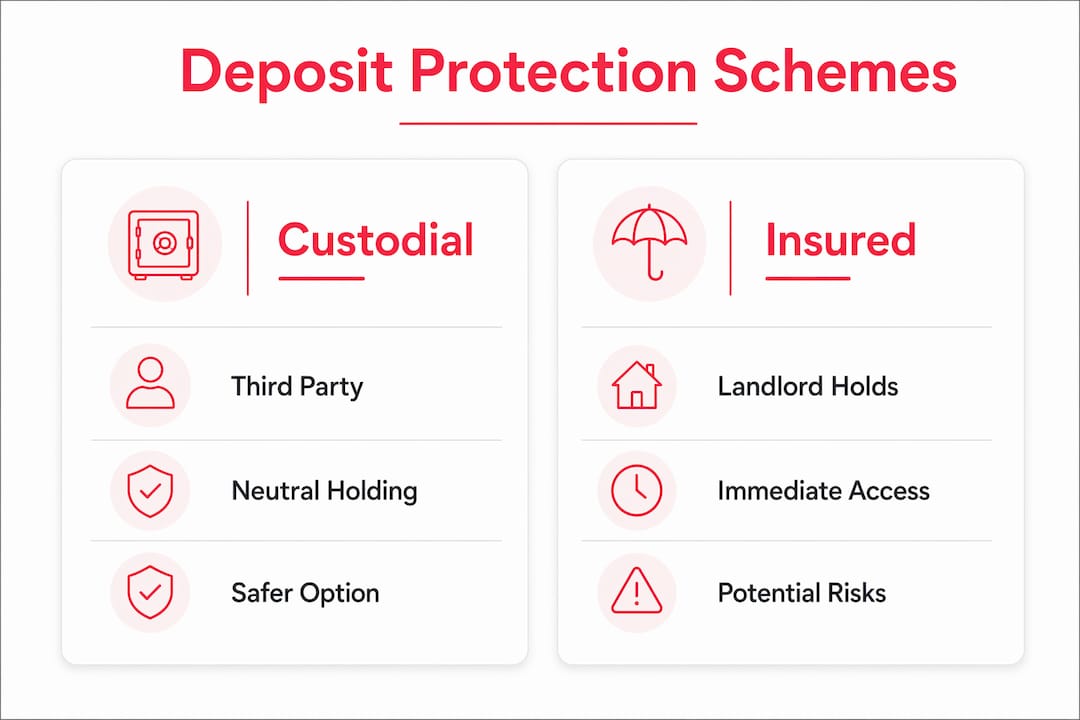

There are two distinct types of scheme, and the difference matters to both parties.

Custodial schemes: The landlord transfers the deposit to an independent scheme, which holds it in trust for the duration of the tenancy. The money sits with the scheme, not the landlord. At the end of the tenancy, both parties agree on any deductions, and the scheme releases the funds accordingly.

Insured schemes: The landlord keeps the deposit in their own account but pays a fee to an insurance provider. The insurance guarantees the tenant will receive their money back if the landlord fails to return it fairly. Organisations such as the Tenancy Deposit Scheme (TDS) operate both types in the UK.

Dispute resolution:TDP schemes provide independent adjudication when landlords and tenants disagree over deductions. An impartial adjudicator reviews evidence from both sides and makes a binding decision. This removes the need for costly court proceedings.

Coverage and scope:Deposit protection covers cash deposits in eligible accounts only. It does not extend to investments, stocks, or cryptocurrencies. This distinction matters if you are ever unsure what a scheme actually safeguards.

Deposit protection also plays a broader role in stabilising the rental market. When tenants trust that their money is safe, they are more willing to commit to longer tenancies. When landlords follow the rules, they avoid significant financial penalties.

Related Topics

#deposit protection for landlords#what is deposit protection#how does deposit protection work#deposit protection insurance#deposit protection explained#understanding deposit protection#what does deposit protection mean#is deposit protection necessary#benefits of deposit protection#deposit protection schemes#understand deposit protection schemes#deposit refund process#deposit security meaning

Related Articles

Pro Tip:Ask your landlord for the scheme reference number on the day you pay your deposit. You can use it to verify protection directly with the scheme, without waiting for paperwork.

What are the legal requirements for landlords and tenants?

The legal framework around deposit protection is clear, and both landlords and tenants have specific obligations. Knowing these rules protects you from costly mistakes.

For landlords, the steps are as follows:

Protect the deposit within 30 days. UK landlords have a 30-day legal deadline to register the deposit with an approved scheme after receiving it. Missing this deadline is a serious offence.

Provide prescribed information. The landlord must give the tenant written details of the scheme used, the amount protected, and how to raise a dispute. This document is called the “prescribed information” and must also be served within 30 days.

Return the deposit promptly. At the end of the tenancy, the landlord must return the deposit, minus any agreed deductions, within 10 days of both parties agreeing on the final amount.

Keep records. Landlords should document the property’s condition at the start and end of the tenancy with a signed inventory and photographs. This evidence is critical if a dispute arises.

For tenants, the obligations are lighter but no less important. You should check that your deposit has been protected by contacting the scheme directly. You should also keep copies of all correspondence, the tenancy agreement, and the inventory report.

Consequences for non-compliance are severe. A landlord who fails to protect a deposit can be ordered by a court to repay the tenant up to three times the deposit amount. They also lose the right to use a Section 21 notice to end the tenancy. These penalties exist to make non-compliance genuinely costly.

Pro Tip:If you never received your prescribed information, do not assume your deposit is unprotected. Check directly with the three government-approved UK schemes: the Deposit Protection Service (DPS), MyDeposits, and the Tenancy Deposit Scheme (TDS).

Custodial vs insured schemes: which is right for you?

Choosing between a custodial and an insured scheme affects who holds the money, how disputes are handled, and what costs are involved. The table below sets out the key differences.

Feature

Custodial Scheme

Insured Scheme

Who holds the deposit

Independent third party

Landlord

Cost to landlord

Free

Annual or per-tenancy fee

Tenant access to funds

Held securely by scheme

Dependent on landlord compliance

Dispute resolution

Handled by the scheme

Handled by the insurer

Risk to tenant

Very low

Low, provided insurance is valid

Best suited to

Landlords who prefer simplicity

Landlords who want to retain funds

Custodial schemes are generally considered the safer option for tenants. The deposit sits with a neutral party from day one, so there is no risk of a landlord spending the money before the tenancy ends. The Deposit Protection Service (DPS) operates a well-known free custodial scheme in the UK.

Insured schemes suit landlords who prefer to keep the deposit accessible, for example to cover emergency repairs. However, the tenant’s security depends entirely on the landlord maintaining valid insurance. If the landlord lets the policy lapse, the tenant’s protection weakens. Some deposit protection schemes are designed specifically for individual savers and tenants rather than business accounts, which is worth checking before you assume coverage applies.

Both scheme types offer the same independent dispute resolution service. The adjudication process is free to use and typically resolves within 28 days of all evidence being submitted.

What practical steps help manage deposit protection?

Good deposit management reduces the chance of disputes and makes the end of a tenancy straightforward for everyone. Here are the most effective steps for both tenants and landlords.

For tenants:

Verify protection within 30 days of paying your deposit by checking directly with the DPS, MyDeposits, or TDS.

Take dated photographs of every room, appliance, and fixture on the day you move in. Store these in a cloud folder alongside your signed inventory.

Report maintenance issues in writing throughout the tenancy. A paper trail shows you acted responsibly and did not cause damage through neglect.

At the end of the tenancy, request a check-out inspection and attend it in person if possible. Disputes are far less likely when both parties walk through the property together.

For landlords:

Use a custodial scheme if you want the simplest, lowest-risk approach. It costs nothing and removes the administrative burden of maintaining insurance.

Serve the prescribed information correctly. A common mistake is protecting the deposit but failing to serve the paperwork within the 30-day window. Both steps are legally required.

Communicate deductions clearly and in writing. Provide receipts or quotes for any repair costs you intend to claim. Tenants are far more likely to accept fair, evidenced deductions than vague claims.

Contact your scheme’s dispute resolution service early if a disagreement arises. Adjudication is free, impartial, and far less stressful than court.

One often-overlooked pitfall is the renewal trap. When a fixed-term tenancy rolls into a periodic tenancy, the deposit protection remains valid. However, if you sign a brand-new tenancy agreement, the deposit must be re-protected under the new agreement. Failing to do this is a surprisingly common cause of penalties.

Key takeaways

Deposit protection is a legal requirement that safeguards tenant funds through government-approved schemes, with landlords facing penalties of up to three times the deposit for non-compliance.

Point

Details

Legal deadline for landlords

Protect the deposit and serve prescribed information within 30 days of receipt.

Two scheme types

Custodial schemes hold funds independently; insured schemes let landlords retain the deposit with insurance cover.

Dispute resolution

Schemes like TDS provide free, independent adjudication to resolve disagreements fairly.

Tenant verification

Check protection directly with DPS, MyDeposits, or TDS using your scheme reference number.

Renewal risk

A new tenancy agreement requires the deposit to be re-protected, even if the same tenant stays.

Why deposit protection is the foundation of a healthy tenancy

I have seen a lot of tenancy disputes, and the vast majority of them share one common thread: poor communication at the start of the let. Deposit protection is not just a legal box to tick. It is the clearest signal a landlord can send that they intend to deal fairly.

What surprises me most is how many landlords still view the prescribed information as an afterthought. They protect the deposit on time but forget to serve the paperwork, and that oversight alone can expose them to a penalty claim months later. The rules are not complicated. The problem is that most landlords only read them once, at the start of their first tenancy, and then rely on memory.

For tenants, the biggest mistake I see is passivity. You paid the deposit, so it is your money. Check that it is protected. Take the photographs. Attend the check-out. These steps take an hour of your time and can save you weeks of stress later.

The deeper point is this: deposit protection schemes work best when both parties treat them as a shared framework for trust, not as a weapon to use against each other. Landlords who communicate clearly about deductions almost never end up in adjudication. Tenants who document the property thoroughly almost always get their money back. The scheme is the safety net, but good behaviour is what keeps you off it.

David Adan - CEO

Rent with confidence using Hauzed

Understanding deposit protection is one part of renting safely. Finding a trustworthy landlord or tenant in the first place is the other.

Hauzed is the rental marketplace built for exactly this. Every landlord and tenant on the platform goes through secure ID verification, and every listing is actively moderated to remove fraud before it reaches you. Whether you are a landlord who wants to list quickly and compliantly, or a tenant searching for a verified home in Dublin, Hauzed makes the process straightforward. Start renting safely with a platform that puts trust at the centre of every transaction.

FAQ

What does deposit protection mean in the UK?

Deposit protection means a landlord is legally required to place a tenant’s deposit into a government-approved scheme within 30 days of receiving it. The scheme holds or insures the money to ensure its fair return at the end of the tenancy.

What happens if a landlord does not protect a deposit?

A court can order the landlord to repay the tenant up to three times the deposit amount as a penalty. The landlord also loses the right to serve a valid Section 21 eviction notice until the deposit is protected.

What is the difference between custodial and insured deposit schemes?

A custodial scheme holds the deposit with an independent third party, while an insured scheme allows the landlord to keep the deposit but requires them to pay for insurance cover. Custodial schemes carry less risk for tenants because the money is held independently from day one.

How can a tenant check if their deposit is protected?

Tenants can check directly with the three government-approved UK schemes: the Deposit Protection Service (DPS), MyDeposits, and the Tenancy Deposit Scheme (TDS). You will need your tenancy start date, deposit amount, and landlord’s name or postcode.

Does deposit protection cover all types of money held at a bank?

Deposit protection covers cash deposits in eligible accounts only, such as current and savings accounts. It does not cover investments, stocks, or cryptocurrencies held through the same institution.